How Medical Insurance Companies Attempt to Deny Addiction Treatment

One of the most common questions I get is “does insurance cover drug rehab”? If you have a similar question, read on because I have going to walk you through the complexity of the answer.

Since 2014 I have watched it get harder and harder for people to use their insurance for alcohol and addiction treatment. You would think, you could just call your insurance company and get the best advice possible. This is not normally the case.

What you need to know about using your PPO or HMO insurance for drug rehab

So you have your medical card out and you want to look into your insurance policy to see what kind of drug and alcohol addiction treatment you can get …. should be easy right? Unfortunately, the motivation of the “customer care” agents at some insurance companies, is self-serving.

At these insurance corporations, the job of the agents is to direct you to the lowest cost option. This doesn’t mean it’s the lowest cost for you. It certainly doesn’t mean it’s the best possible care you can get. In fact, the abusive and dangerous actions of one insurer this week has prompted me to write this article.

You pay thousands of dollars more for a PPO Insurance policy, so don’t be tricked into settling for HMO drug rehab treatment.

PPO Insurance Policies Compared to HMO Policies

PPO insurance policies are far more expensive than HMO policies. The main reason individuals and employers purchase PPO policies is quality. The attractiveness of this option is the personal choice you receive to get the best care available. This typically means you don’t need to wait for an appointment and you can pick your provider.

Medical insurance should pay for substance abuse treatment. Addiction is just as much as a disease as diabetes, liver failure or dementia.

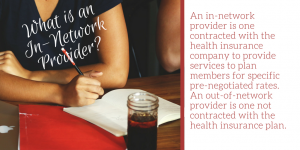

With a PPO insurance policy, you should be free to go to (theoretically) to any medical service provider you want. So why is it when you call your insurance company, they try to convince you to go to an “in-network provider”? You, after all, are paying double or triple the premium.

You got a PPO policy for this very reason — you want to be able to pick your own provider outside of the insurance companies’ network.

Fact’s that No one will Tell You. Don’t Get Tricked by In-Network Options

If you don’t pay careful attention to your options, this is what could happen.

You call your insurance company to get information about your out-of-pocket costs for drug rehab. They act so nice telling you that you can save money by going “in-network”. What they really mean is that they (the insurance company) will save money if you go in-network. Remember you pay a lot extra every month so you can you can have the privilege of choice. Choose the best alcohol or drug rehab that is right for you.

First-Hand Experience with Using Insurance for Addiction Treatment

Yesterday I was helping a parent (of a drug addict) with an employer-paid PPO insurance policy. He asked me to recommend a treatment center. I chose a couple of centers that I knew were a good match for him. This twist is that his insurance company recently adopted a new policy.

Hang with me, this gets a little sticky.

It states that in order for one of their insured to get into substance abuse treatment the insured person (the son) must call the customer service department of the insurance company and give them permission. This “permission” is for the specific treatment center to verify coverage. So yesterday morning the father called his insurance company to authorize them to release his insurance benefit information. The customer service agent tried to talk him out of his choice of treatment centers and suggested they knew a better one.

Our poor fellow had a PPO policy and wanted an out-of-network choice but the insurance company agent berated his decision. The agent made all sorts of negative comments about the facility I chose and then insulted me (I’m just the guy trying to help him).

Our poor fellow had a PPO policy and wanted an out-of-network choice but the insurance company agent berated his decision. The agent made all sorts of negative comments about the facility I chose and then insulted me (I’m just the guy trying to help him).

This was done with no investigation of the facts. They went “on and on” how they would save money by going to an in-network drug treatment center. Well, that was either a lie or the insurance company never bothered to look at the clients’ account. I know this because the client had spent a significant amount of money last month on “out-of-network” medical treatments. They had met their out-of-network deductible and their out-of-pocket maximum.

The client had not seen or spent any money in-network. Therefore, the out of network care would be less expensive to the client and better treatment than the in-network facility.

Our Pursuit of Addiction Treatment Continues…

You would think the story ended there but it didn’t — it got worse. Although the client authorized the insurance company to allow two treatment centers to verify his benefits, the insurance company told the two treatment centers it wasn’t authorized yet.

So now, one day has already passed and the client was denied drug treatment. The client called the company back and they gave him a stupid statement about being “in the file” now.

However, it was past the insurance company verification hours, so he will have to call back the next day.

Unfortunately, when the two treatment centers finally got through to the benefits line, the company again said they had not been authorized yet. So now for two days drug treatment “per the policy” is effectively denied. I suggested as a backup we submit a benefit check for an in-network rehab facility. This went through in about an hour. Unfortunately, the care offered at the in-network facility does not rival the out-of-network facilities. And, the cost was going to be greater to the client.

The Real Fraud of Insurance For Addiction Treatment

In my opinion, this is insurance fraud on the part of the insurance company. Their stall technique may cause unnecessary overdoses and deaths. When people seek addiction help it typically occurs while some crisis is going on. Minutes matter when a person needs rehab treatment, time is of the essence and its life and death. More people die from addiction than are killed in car accidents or by guns.

Don’t panic when you get an INSURANCE LETTER that looks like bad news!

Okay, so your loved one is in treatment, the facility has admitted them, and you think your worries are over. Then an insurance letter comes in the mail that says your loved one is approved for ONLY 2 to 4 days of drug or alcohol treatment. You panic because they need 60-90 days care. Don’t panic these letters are normal even for drug rehabs and treatment centers that tout themselves as providing up to 90 days of treatment.

At the start, insurers typically approve addiction treatment in 2-4 day intervals. This generates a lot of paperwork and a lot of letters. Insurance companies require that drug treatment facilities submit substantial documentation, medical reports, lab tests etc. before they will approve any claim. Once they approve a claim for a fixed period of time and a certain level of care, the process starts all over again to extend the care.

The treatment center must document and demonstrate every service performed. This is a process an established drug rehab or addiction treatment center is very familiar with. They are happy to get these letters versus denials.

Detox Programs and Inpatient are Billed Differently

Once a client is through the drug or alcohol detox (which is the most expensive level of care) and moved to a different level of care, the approval letters start coming for longer and longer periods of time. Typically you will see 5 -10 days pass per letter or more.

Denial of coverage letters are common and they don’t mean your loved one will be discharged from treatment!

Denial of treatment or denial of a treatment payment letter can typically be caused by the drug and alcohol treatment center not filling out their claim request properly. If an “i” is not dotted or a “t” is not crossed, insurance companies will deny claims. Typically the treatment center will get the same letter as the insured.

When the drug treatment center receives these types of letters they work with their billing department to remedy the issue. In my opinion, insurance companies staff are trained to look for ways to deny claims. To me, this means they would rather deny a claim for substance abuse addiction rather than approve it. This does not mean your loved one is necessarily going to get kicked out of treatment. Don’t panic if you get one of these letters.

Action Step

This is the time you call your treatment coordinator and send them a copy of the letter you receive. They can communicate directly with the drug treatment center and get down to what the real issue is. Rarely does a well-established rehab make a mistake and admit a client that they will not get paid for.

In those rare occasions where a mistake is made an ethical established rehab facility will continue to treat the client.

There are legitimate reasons for an insurance company to deny treatment that do arise.

Recently a client who had been to treatment many times before knew his insurance was not a quality policy. This client lied and exaggerated their drug use (normally it’s the other way around under disclosing). When the rehab facility gave the client a drug test the test showed barely any drugs in the clients’ system. The client was turned down by his insurance company for detox treatment. Lying on an intake form or call is a legal reason for insurance companies to deny benefits. This is also a legitimate cause for a drug treatment center to discharge a client.

On the other side of the coin, if the client lies on the intake call and gets to rehab and they find that he uses additional substances than stated at intake, this could also cause problems. In some situations that facility may not be medically qualified to treat the client. A good treatment coordinator can usually get the truth out of someone seeking addiction treatment and avoid these issues.

Exceptions rather than the rule

There are drug and alcohol addicts that use treatment centers like hotels and bounce in and out of them. If your loved one has been to multiple rehabs in the last 12 months make sure you disclose these facts to your treatment coordinator. This way, they can find you the best fit.

Is it better to go with an In-Network Drug rehab or an Out of Network Treatment Center?

People always want to know which is the best choice provider of insurance for addiction treatment. When you need substance abuse treatment services, is a facility that is “in-network” with your insurance company or a treatment center that is “out of network” with your insurance company better?

As a rule of thumb if a treatment facility is “in network” with an insurance company they tend to have a waiting list, and the amount of time a person stays is drastically reduced.

The reason for that is “in-network” facilities get referrals from the insurance companies which keep them full. They don’t need to offer financial hardships because they are full. In my opinion, the length of stay is shorter because they want to keep the insurance companies happy by reducing the cost of care to the insurance company. I always suggest using an addiction treatment center “out of network” if you can. This way you will most likely get better care.

Most substance abuse and mental health treatment centers are not in-network with most insurance companies.

Getting an experienced treatment advocate to help you find a treatment center and negotiate with the treatment center and your insurance company will save you time and money. Often a treatment advocate will greatly enhance the quality and length of treatment received.

If you are looking for your insurance company to pay for drug or alcohol treatment, review your “Summary of Benefits” online before you start looking for a drug rehab or treatment center. The first of each year insurance companies often change policy benefits so that the insurance policy you have may have worked for treatment one or two years ago may not work today.

You need to check your insurance policy.

If you have received your insurance from your employer and it is a PPO policy your options for treatment are much better. This is compared to what’s available from insurance received from the HealthCare.gov website. State insurance policies are typically the worst since they offer very few choices.

Action Steps When Looking at Insurance for Addiction Treatment

So the first thing you want to look for (even if you have a PPO insurance policy) is to verify what the “out-of-network benefits” are for mental health and substance abuse. There are three specific items that will determine what portion of the treatment cost you may need to pay for if any.

- What is your out-of-network deductible? Most policies have a different deductible for in-network providers than they do for out-of-network providers. Deductibles on good employer policies typically range between $500 and $2,500. Your actual deductible due can be less than the stated deductible if you have been to the doctor this year. Whatever the balance is of the deductible you will have to make arrangements to pay that to the treatment center.

- What is the co-pay or what percentage does the insurer pay? Your insurance policy will likely have a percentage of care that you are responsible for. Typically it runs from 10% to 50% of the medical cost. Before you start taking out the calculator read ahead. The next item may be of a relief because it will tell you most likely what your share of the treatment cost will be if anything.

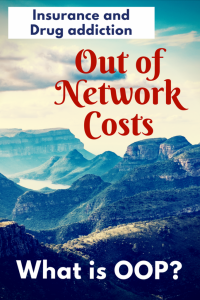

- What are the maximum “OOP” out-of-pocket costs? Besides your deductible, your policy will have a dollar amount that is known as the maximum out-of-pocket. This is an important number because it represents how much money you most likely will have to either pay or arrange financial aid for, to pay for treatment. If your OOP is $10,000 and you have paid nothing towards your deductible most likely you will have a cost not covered by insurance of $10,000.

Do not be discouraged if the amount seems unaffordable as some treatment centers offer financial hardship arrangements if you can’t afford your deductibles and co-pays.

Do you have a question for the author of this article? Just click on the chat box below and submit your inquiry. You’ll get a response within 24-hours.

About the Author

Bruce Berman personally has assisted several hundred people into treatment for alcohol, substance abuse, and dual diagnosis. He has maintained continuous recovery from various addictions since September 1989. Besides himself, he has placed his own children, employees, family members, friends and other loved ones into various treatment programs. Whether you are struggling with addiction or a loved one is most likely the author has dealt with a similar situation in the past. Bruce is a father of four children ages 9 to 31 and happily married to his wife Victoria who has also been in recovery since November 1995. Together Bruce and Victoria run 800 Recovery Hub a company that specializes in placing people in need of treatment into the best treatment center they can.

DISCLOSURE

Bruce Berman is not a medical doctor, holds no degrees or licensees in addiction and has no formal education in treating addiction. He relies solely on his personal experience gained in attending and participating in over 10,000 hours in various 12 step meetings since 1989 as well as the experience he has working with addicts and their families since 1989.